The risk of US interest rate normailisation affecting China (via capital outflows) could be limited because of the large Sino-US interest rate spread (more than four percentage points at the time of writing), the lack of free capital flows in and out of China, and the lack of substitutability between Chinese and US assets. In other words, the conditions for “uncovered interest rate parity” do not apply to China. These arguments still stand, despite the prospect of Chinese interest rate cuts in the short-term.

What about the risk to China’s growth from the withdrawal of foreign capital as the US quantitative easing (QE) ends? Some analysts have argued that China financed most of its economic recovery from the global financial crisis with imported capital. They cite the fact that cheap money created by the US Fed’s QE policy flooded offshore centres, mainly Hong Kong, and then went to China in the form of carry trades. These QE-induced funds were first converted into Hong Kong dollars, which is pegged to the US dollar, and then invested in renminbi (RMB)-denominated high yield financial products issued by mainland Chinese companies in the offshore Hong Kong (or CNH) market.

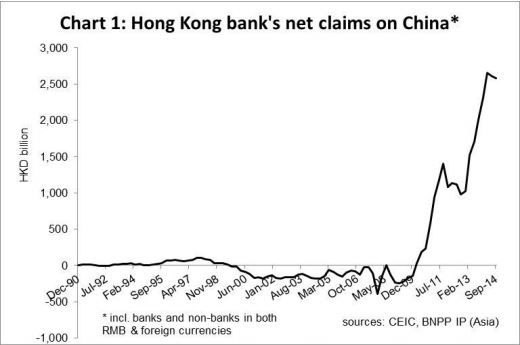

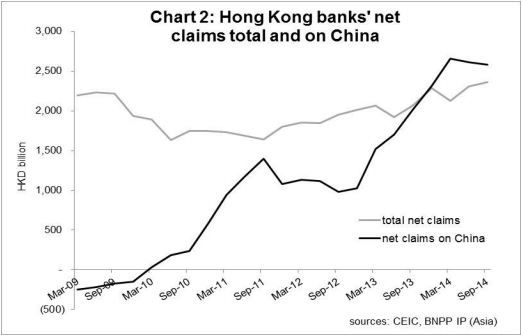

Official data seems to support this argument. Hong Kong banks’ net claims on China have soared since 2010 to unprecedented amounts (Chart 1). As of Q3 2014, the latest data available, international claims and liabilities of Hong Kong banks were HKD9.4 trillion and HKD 7.0 trillion, respectively, resulting in HKD2.4 trillion of net claims. Meanwhile, net claims by Hong Kong banks on China amounted to HKD 2.6 trillion, up from almost zero in 2009. The fact that net claims on China by Hong Kong banks have risen exponentially in recent years while total net claims are almost equal to the net claims on China suggests that the bulk of Hong Kong banks’ foreign lending had funded China’s growth (Chart 2).

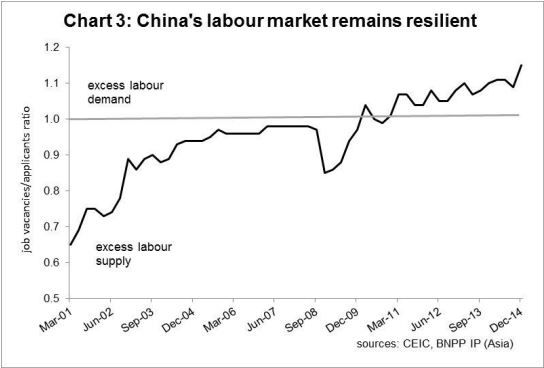

The key risk to China’s growth is not the end of the US QE, but weak aggregate demand. The relevant question is: where is the pain threshold for China’s growth and what will be the catalyst for Beijing to resort to a significant economic bailout? We have argued that it would not be inflation because there is none, or a credit event in the system since Beijing still has a selective “implicit guarantee” policy that protects systemic confidence. The key to answering the growth-pain threshold question lies in China’s labour market.

Beijing will tolerate slow growth for the sake of structural reforms as long as employment remains resilient. This has been the case so far, despite slowing economic growth,. China’s labour demand-to-supply ratio has remained above one since 2009, suggesting tight labour market conditions (Chart 3). The economy has grown in size, with the labour-intensive services sector now accounting for a larger share, hence demanding more labour, than the manufacturing sector. Meanwhile, growth of the labour force has decline due to an ageing population.

So where exactly is this threshold? Econometric modeling cannot provide any precise answers due to imperfect data and unstable structural parameters in the economy. The market’s estimates range from a growth rate of 5% to 6.5%. This means that Beijing has a rather high growth-pain threshold, giving it the leeway to purse structural reforms at the expense of growth.

Chi Lo, Senior Economist, BNPP IP